Advanced Content

How the Central Bank Creates Money

Creating Central Bank Reserves

Let’s start by seeing how the Federal Reserve creates the electronic money that banks use to make payments to other banks. Central bank reserves are one of the Three Types of Money and are created by the central bank in order to facilitate payments between commercial banks.

In the following example, we will show how the central bank creates central bank reserves for use by a commercial bank – in this case Bank of America. Initially, the Federal Reserve’s balance sheet as it appears here (this is a simplified example where we’ve only highlighted one particular transaction).

BOA’s shareholders have put up $10,000 of their own money which has been invested in government bonds. So BOA’s balance sheet looks like this.

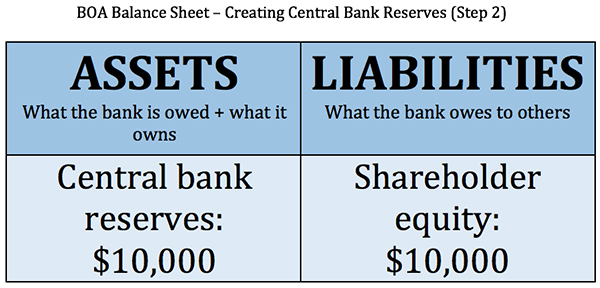

As a customer of the central bank, BOA contacts the central bank and informs them that they would like $10,000 in central bank reserves.

For the purposes of this example we will assume that the Federal Reserve purchases the Treasury Bills from BOA outright. Once the sale is completed the Federal Reserve has gained $10,000 of T-Bills, but it now has a liability to BOA of $10,000, which represents the balance of BOA’s reserve account.

The Federal Reserve’s balance sheet has now ‘expanded’ by $10,000, and $10,000 of new central bank reserves have been created, effectively out of nothing, in order to pay for the $10,000 in T-Bills.

However, from the point of view of BOA’s balance sheet it has simply swapped $10,000 in T-Bills for $10,000 in reserves.

BOA’s balance sheet has not expanded at all; it has simply swapped one asset for another, without affecting its liabilities. BOA can now use these reserves to make payments to other banks.

The central bank could alternatively lend BOA the reserves. In this case the assets side of the central bank’s balance sheet would show a $10,000 loan to BOA rather than $10,000 of T-Bills. The BOA balance sheet would show the new reserves as an additional asset on top of its holdings of T-Bills and its obligation to repay the loan as an additional $10,000 liability.

Sale and repurchase agreements (Repos)

The other, more short-term method by which the Federal Reserve creates reserves is through what is known as a sale and repurchase agreement (a repo), which is similar in concept to a collateralized loan. Essentially, BOA sells an “interest” in an asset to the central bank (for instance a T-Bill) in exchange for central bank reserves, while agreeing to repurchase that interest in the asset for a specific (higher) price on a specific (future) date. If the repurchase price is 10% higher than the purchase price (i.e. 10% higher than $10,000 = $11,000) then the ‘repo rate’ is said to be 10%. A repo transaction has different accounting rules from an outright sale. The Federal Reserve balance sheet would not show the T-Bills as the asset balancing the reserves, but it would show the value of the interest in the T-Bills (valued at the $10,000 paid, not the $11,000 promised). BOA would retain the T-Bills on its balance sheet in addition to the central bank reserves, but record as an additional liability its $10,000 obligation to complete its end of the repurchase agreement. The extra $1,000 does not appear on either balance sheet but, when paid, is recorded as revenue (profit) for the Federal Reserve and an expense (loss) for BOA.

Repo operations are used for fine tuning the amount of reserves in the system so that the Fed can hit its target Fed Funds rate. If the interbank interest rate (Fed Funds rate) is too high, it adds reserves to the system. If it’s too low, it takes them out with “reverse” repos. This fine tuning takes place within the Fed’s “corridor” system, by which it puts a floor and a ceiling on the price of reserves. It does this by controlling the rate of interest it pays on reserves, as well as the interest rate it charges banks to borrow in an emergency (it charges a premium interest rate on reserves it lends through the discount window).

This ‘corridor’ allows the Fed to set the interest rate at which banks lend to each other on the interbank market. For example, if the rate it pays on reserve deposits is 4%, and the rate it charges on emergency lending is 6%, a bank will never lend reserves to another bank at a rate of interest below the rate it could receive from simply holding its reserves in its reserve account at the Fed (4%), nor borrow reserves from another bank at a rate of interest higher than it could borrow from the Fed’s discount window (6%). Because of this, the interest rate banks will be willing to lend reserves to each other on the interbank market will be somewhere between 4 and 6%. Then the Fed uses repo operations to get the interest rate right where it wants it, say 5%.

How Commercial Banks Acquire Cash from Central Banks

The process by which commercial banks acquire cash from the central bank is similar to that used for acquiring reserves. It is probably easiest however to think of it simply as commercial banks withdrawing their central bank reserves in the form of cash for their vaults. Initially, the Federal Reserve’s balance sheet appears as shown here.

And BOA’s balance sheet shows an asset of $10,000 in Central bank reserves and liability of $10,000 shareholder equity.

If BOA decides it is expecting an increase in demand for cash then it may wish to exchange some of its (electronic) central bank reserves for (physical) cash. The process by which it does so is very simple – BOA simply exchanges $10,000 of its central bank reserves for $10,000 cash.

The Federal Reserve’s liabilities change from $10,000 in BOA’s reserve account, to $10,000 of ‘cash outstanding.’

Meanwhile, BOA’s assets have changed from $10,000 of central bank reserves, to $10,000 in cash.

Note that neither balance sheet has expanded or contracted; it is just the nature of assets and liabilities that have changed. When the cash is worn out, damaged, or not needed anymore, the transaction is reversed and BOA simply sells back the cash to the Federal Reserve at face value, receiving $10,000 in central bank reserves in return.